COUNTY NEWS RELEASE

Los Alamos County property owners will be receiving their 2021 property tax bills over the next couple weeks. Most will see relatively little change from last year, but for some there may be a big surprise.

Imagine yourself in a home you just purchased. You settle in and maybe even do some fix-up to make it “your own.” Then comes the first week of November and you receive your first property tax bill in the mail. You tentatively open the envelope and suddenly realize that WOW, it’s not that bad. In fact, your tax might be much lower than anticipated.

Now fast forward one year to when you get your second property tax bill. No big deal, you think. You open the envelope with no trepidation and — OMG! Taxes went up 50%, 60%, 70% or more. How can this happen?! Well, you just got hit by the unintended consequences of a well-intentioned State Law. The consequence is called “tax lightning.”

Years ago, as more people moved into New Mexico, many older residential neighborhoods were becoming gentrified, which caused property values to increase. Lower income property owners, some of whom owned property that had been in their family for generations, were being taxed out of their homes. To remedy this situation, the state legislature passed a law limiting yearly residential assessment increases to 3%, regardless of the property’s actual market value.

The law capping annual assessment increases has several exclusions, among them are the portion of a home that is renovated. (Non-residential property, such as commercial or vacant land regardless of zoning, is also excluded from the cap). The exclusion that hits home purchasers the hardest, however, is home ownership transfers. When ownership of a home transfers to a new owner, the assessment is set to market value on January 1 of the following year. This means that the year in which a home is purchased, the property tax is based on the previous owner’s capped assessment value. On January 1 of the following year, the assessment jumps to the market value.

Starting in 2007, the market value of Los Alamos homes fell. Although assessment increases are capped, assessment decreases have no limit. In late 2015, the housing market turned upward, and sales prices have increased every year to current double-digit rates. As a result, approximately 90% of residential assessments in Los Alamos are capped. Those homeowners do not see a dramatic increase in their property assessment. Tax lightning only impacts the purchaser of residential property.

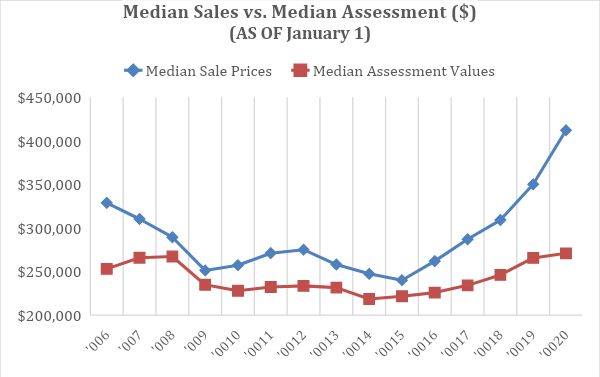

The following graph illustrates the impact of tax lightning. Looking at median residential sale prices and median residential assessment values on January 1 of each year from 2006 through 2020, the graph shows the disparity between the two values.

From 2006 through 2020, the disparity between median sales price versus median assessment value ranged from 7.03% to 52.12%. What does this mean in real dollars to the taxpayer who purchased a home? Let’s say you purchased a home in 2019 at the median sales price of $350,000. Your tax bill would have been based on the previous owner’s assessment of $265,585. The taxes would be $2,205.77.

The following year, on January 1, 2020, your assessment would adjust to market value, $412,000. The November 2020 tax bill will be $3,369.06, a 52.74% increase! It is small comfort knowing that going forward increases in your assessment values might be capped.

There are other unintended consequences from the law limiting residential assessment increases. The NM Counties Assessors Affiliate, along with the NM Association of Realtors have worked over the years to have the NM State Legislature address the law’s shortcomings, but without luck. In the meantime, home purchasers will continue to have the November surprise.

Lastly, what does the increase mean to revenue for the taxing entities? Not much. The NM Department of Finance Administration annually sets property tax levies throughout the state using a yield control formula to stabilize revenue. Those levies generally have an inverse relationship to property value. As property values increase, tax levies are reduced and vice versa.